Market Risk

The Centerprise EP Market Risk module keeps fund managers and risk officers on top of current and historical exposures and provides tools to assess impacts of potential future scenarios.

Key features:

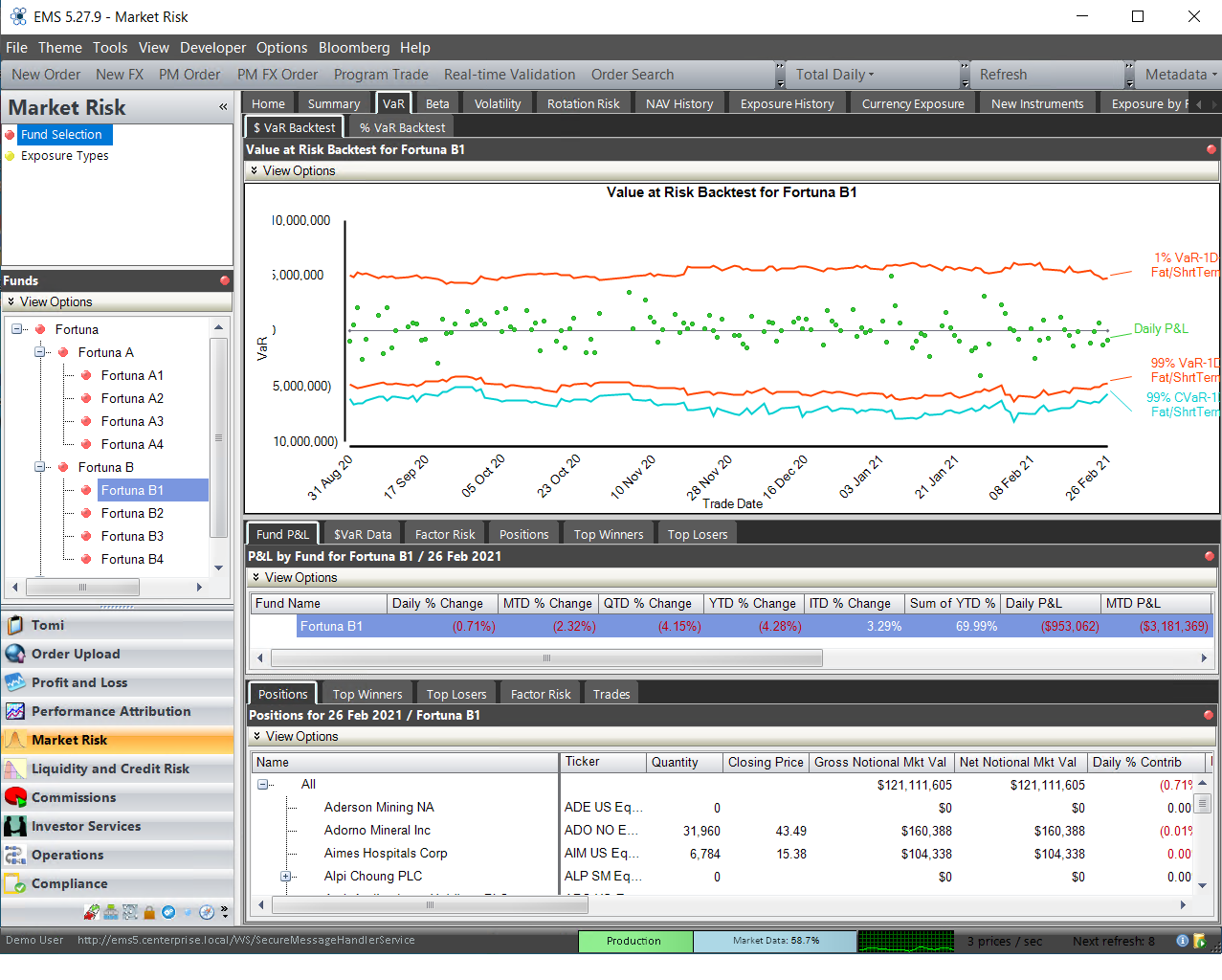

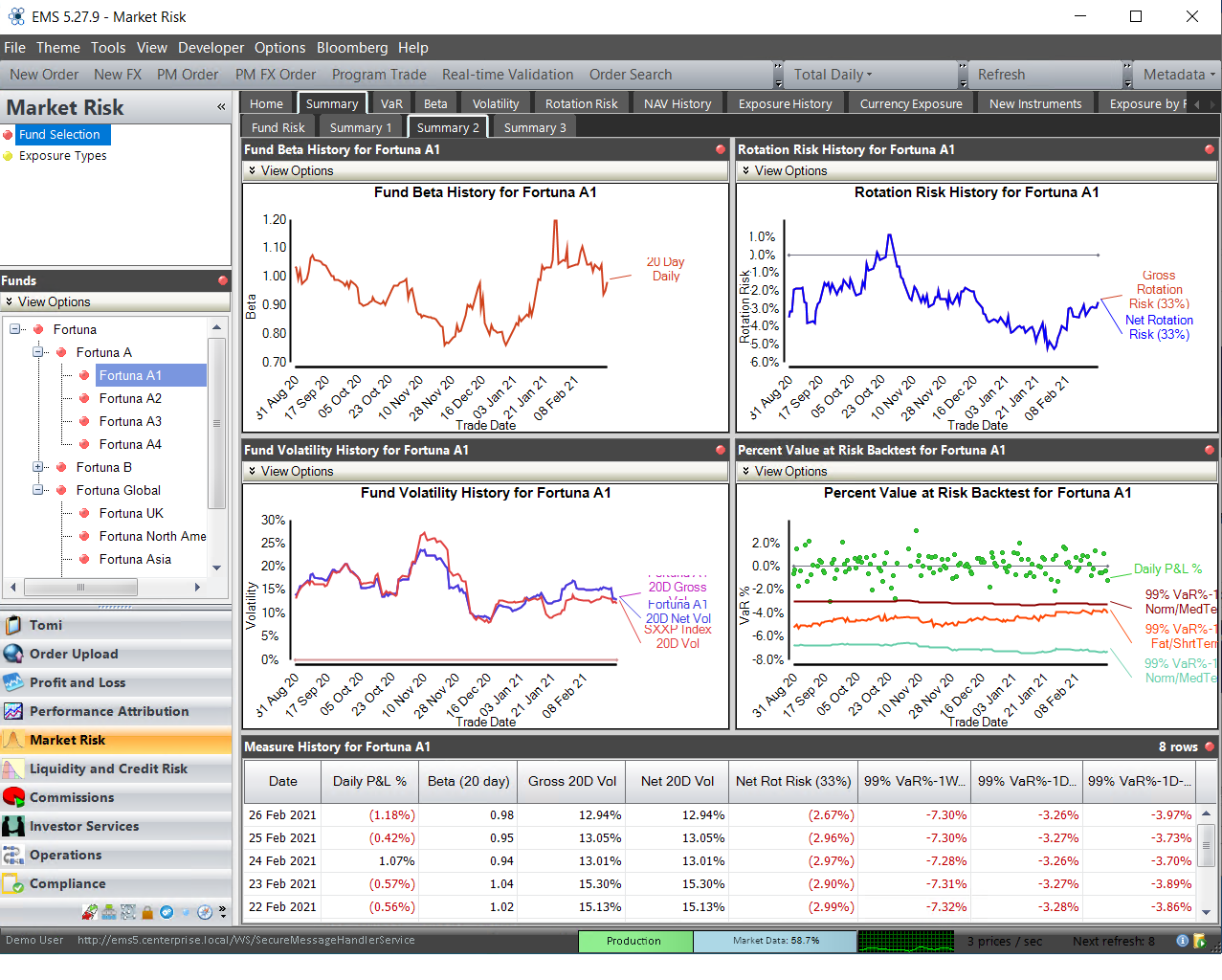

- Support for a broad range of risk exposure measures including net, gross, volatility, betas, and stress testing

- Full Monte Carlo VaR with integrated back testing against experienced P&L

- APT factor analysis statistics

- Various basis risk measures

- Customizable stress test scenario generation

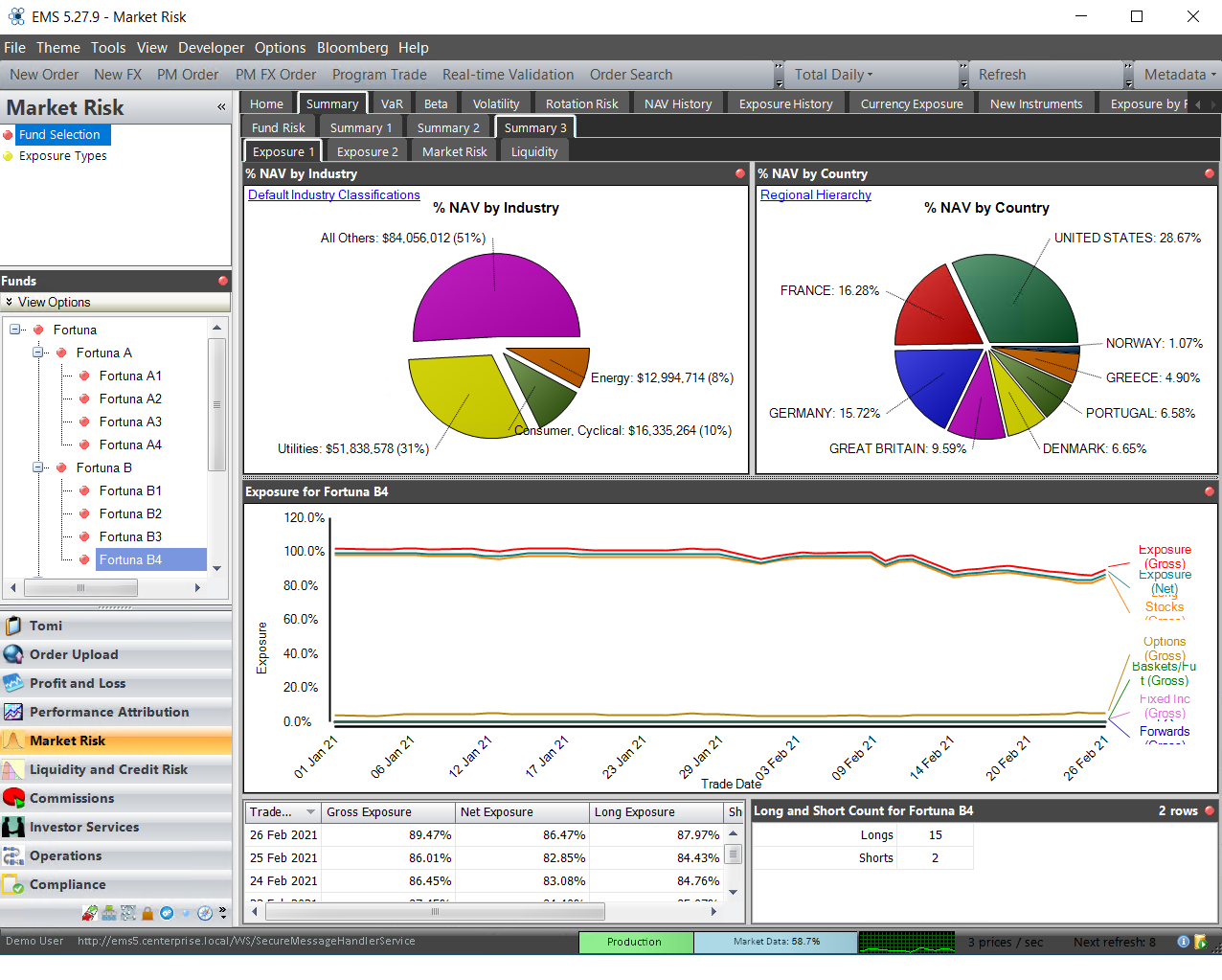

- Comparison of portfolio sector or security weights to a benchmark with full tracking of historical changes

- Monitoring of new instruments traded